Since the beginning of the year, the Federal Reserve (FED) has injected nearly three trillion dollars directly into the U.S. economy with decisive action and has another trillion dollars in the pipeline.

In contrast, the European Central Bank’s (ECB) efforts have reached barely half that amount, primarily aimed at supporting banks, seemingly diverging from the path taken by the FED.

What implications might these distinct economic strategies hold for Europe’s economic future?

Growth or Inflation: A Tale of Two Central Banks

At the onset of 2020, both central banks faced relatively similar starting positions. The FED’s assets stood at $4 trillion, while the ECB held €4.6 trillion.

Between March and May 2020, the FED’s balance sheet surged to $7.1 trillion. A portion of this economic stimulus reached American citizens in the form of checks for $1,200. Having acted decisively then, another trillion-dollar stimulus package, potentially including more direct payments, is now anticipated.

Conversely, the ECB remains focused on its primary—and seemingly singular—objective: ensuring price stability, i.e., controlling inflation. While it injected €1.3 trillion into European banks, this capital appears directed towards addressing immediate financial strains rather than building a future or securing the present for citizens struggling to make ends meet.

It appears Europe might be willing to risk economic disintegration rather than tolerate inflation. Is the memory of interwar hyperinflation that potent? What benefit is inflation control to an economy that is not functioning for its people?

“Whatever it Takes”? A Question of Urgency

Following the 2008 crisis, the ECB took four years to react with Draghi’s famous phrase, “Whatever it takes.” This pledge to do “whatever it takes” translated into purchasing public debt almost without limit, granting Eurozone countries a grace period that could have been used for structural reforms—reforms that were largely not implemented.

Could Germany have sold as many automobiles in recent years without the large, semi-captive market of Southern Europe? What has been the real impact of the hundreds of billions spent by European governments on bank bailouts? How long has Spain been aware of the unsustainability of its pension system and the imbalances within its public administration? Europe may be deluding itself by thinking its economy is comparable to the U.S. economy.

Two Central Banks, Diverging Outlooks on Currency Exchange Rates

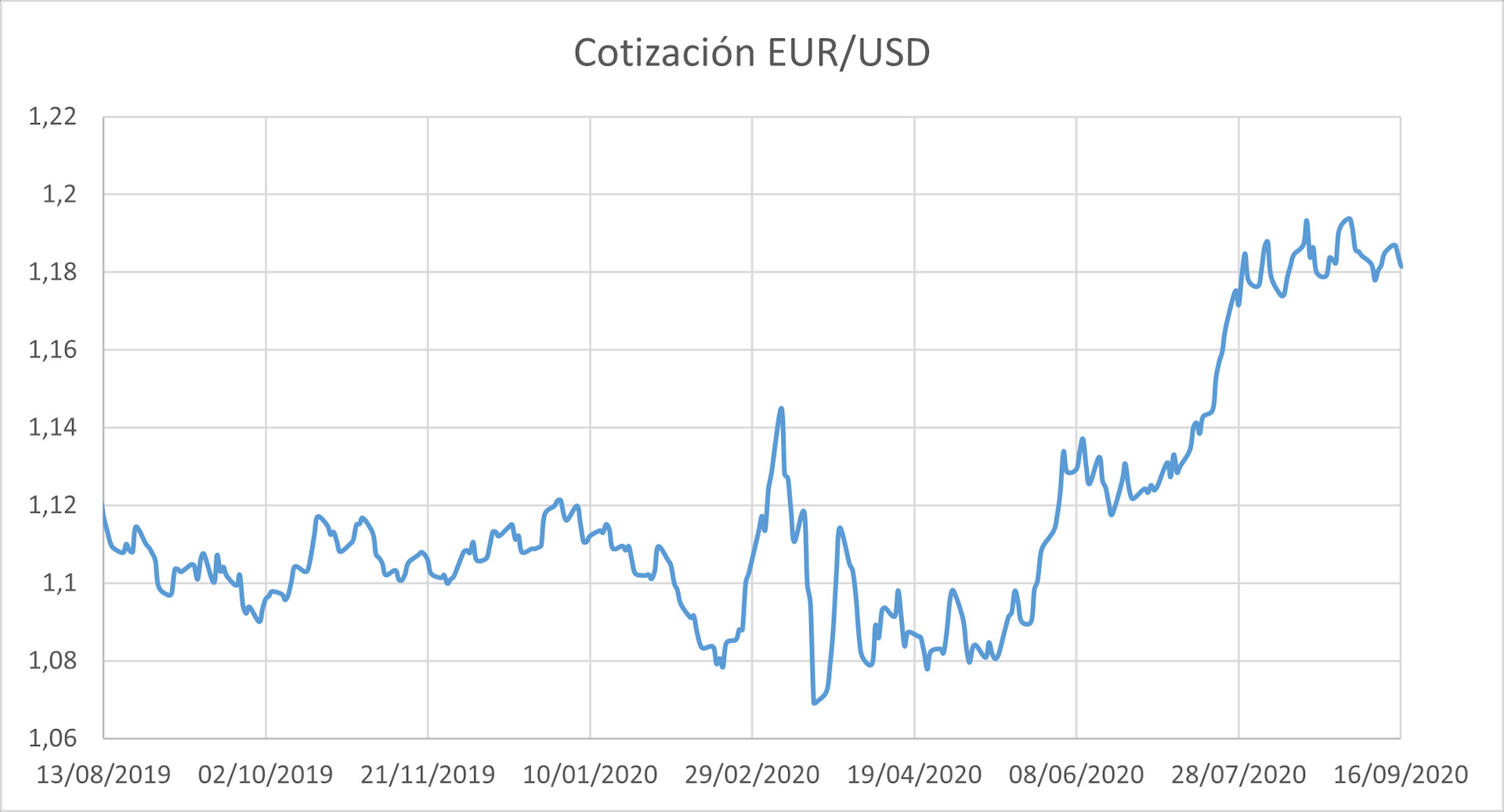

The relative increase in the number of dollars compared to euros is one factor contributing to the euro’s recent appreciation against the dollar. From February to September 2020, the euro-dollar exchange rate shifted from €1.08 to €1.18 per dollar.

Euro to Dollar Exchange Rate August – September 2020

Euro to Dollar Exchange Rate August – September 2020

A strong euro makes European products relatively more expensive compared to American goods, favoring imports from the United States and disadvantaging European exporters.

This situation moves the Eurozone further away from inflation but harbors dangerous pitfalls. Consumption declines, average wages decrease, and unemployment rises. What is the point of strengthening the euro if EU citizens do not have euros in their pockets or face economic hardship?

Jerome Powell, Chairman of the FED, announced weeks ago that he would continue the policy of economic stimulus in the United States. In his address, he indicated that inflation is not as critical as the need for reforms to secure the long term.

The world has changed, social inequality is rising, and action is imperative. Last week, his counterpart at the ECB, Christine Lagarde, adopted a more cautious stance: the ECB is still studying the possibility of making the inflation target more flexible.