When traveling to Europe, particularly Italy, understanding foreign transaction fees and exchange rates is crucial for managing your budget. Let’s break down the potential costs of withdrawing 800 Euros In Dollars, comparing different financial institutions and exploring how to minimize expenses.

When considering accessing your funds in Europe, you’re likely looking at options like using your existing bank cards at ATMs or opening an account with a financial institution that offers better international rates. The original poster in a forum was exploring these very options, specifically comparing credit unions to a large bank, PNC, to withdraw 800 euros while in Italy. They were trying to understand the fees involved and find the most cost-effective solution.

Comparing Credit Union and PNC Fees for 800 Euros

The user initially investigated two local credit unions and PNC Bank to determine the costs associated with withdrawing 800 euros in Italy. Here’s a breakdown of their findings:

Credit Unions:

- Foreign Transaction Fee: Both credit unions quoted a 1% foreign transaction fee.

- Exchange Rate Uncertainty: Neither credit union could provide an exact dollar amount for 800 euros at the time of withdrawal. This is because the final cost depends on the exchange rate at the moment of the transaction and any fees imposed by the Italian bank’s ATM (Bancomat).

- Customer Service: One credit union offered 24/7 phone service but lacked detailed knowledge of international fees. The other had limited hours but offered more helpful, albeit still uncertain, information.

PNC Bank:

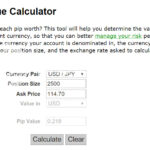

- Foreign Transaction Fee: PNC charges a 3% foreign transaction fee when using a debit card at a Bancomat in Italy.

- Exchange Rate Plus Fee: Using the example provided, at an exchange rate where 1 euro equals approximately $1.09, PNC would charge around $1.123 per euro (exchange rate + 3%).

- ATM Transaction Fee: PNC charges a $5 fee for each foreign ATM withdrawal, but their account reimburses the first two foreign ATM transaction fees per billing cycle.

- Domestic ATM Fees: For comparison, PNC charges $3 for using non-PNC ATMs in the USA (also with reimbursement for the first two transactions) and non-PNC ATMs in the USA might additionally charge around $2.95.

Cost Comparison for 800 Euros:

Based on the information gathered, the user calculated the following:

- PNC ATM Withdrawal Cost: Approximately $24 more than a credit union for withdrawing 800 euros.

- PNC Pre-ordering Euros Cost: $128 more expensive than using a credit union to obtain 800 euros.

This significant difference highlights the potential savings when choosing a financial institution with lower foreign transaction fees, especially for larger withdrawals like 800 euros.

Understanding Potential Italian Bank (Bancomat) Fees

A key question raised by the user is regarding the fees charged by Italian banks when using their ATMs, often called Bancomats, particularly at locations like Rome Airport. Unfortunately, these fees are often not transparent and can vary. It’s challenging to determine the exact fee beforehand as it is imposed by the ATM operator in Italy, not your US bank or credit union.

These fees can add to the overall cost of withdrawing cash abroad. While some ATMs might have lower or no fees, others, especially those in tourist-heavy areas like airports, could impose additional charges. It’s always advisable to check the ATM screen for any fee disclosures before finalizing your transaction.

Alt text: A close-up comparison image showing a US one dollar bill positioned next to a Euro ten note, emphasizing the visual difference between US and European currencies for travelers.

Justifying a Local Credit Union Account for European Travel

The user also questions the value of opening an account at a local credit union, considering their limited operating hours. However, for travelers planning trips to Europe or engaging in international transactions, a credit union account can offer considerable benefits:

- Lower Foreign Transaction Fees: As illustrated in the comparison, credit unions often have significantly lower foreign transaction fees (like 1%) compared to larger banks (like PNC’s 3%). This can lead to substantial savings, especially for larger withdrawals like 800 euros.

- Potentially Better Exchange Rates: While exchange rates fluctuate, credit unions, due to their member-focused structure, may offer slightly more favorable exchange rates compared to large commercial banks.

- ATM Fee Reimbursements (Potentially): Some credit unions may also offer ATM fee reimbursements, although this wasn’t explicitly mentioned in the original post for these specific credit unions. It’s worth inquiring about.

While limited customer service hours might be a drawback for some, the potential cost savings on foreign transaction fees, especially when withdrawing sums like 800 euros, can easily justify opening and utilizing a credit union account for international travel. For frequent travelers or those planning extended stays in Europe, the savings can accumulate significantly over time.

In Conclusion

When planning to withdraw 800 euros in dollars for a trip to Italy, opting for a credit union over a larger bank like PNC can lead to considerable savings due to lower foreign transaction fees. While Italian ATM fees can be unpredictable, the initial savings from using a credit union provide a solid financial advantage. Consider opening an account with a credit union if you anticipate needing euros and want to minimize currency exchange costs for your European travels.