In recent times, the U.S. dollar has surged to heights not seen in two decades, a significant shift in the global economic landscape. This ascent is largely attributed to the United States Federal Reserve’s aggressive interest rate hikes since March 2022, a response to persistent inflation. These higher rates, coupled with the perceived stability of the U.S. economy, have amplified the dollar’s attractiveness, triggering a “flight to safety” among international investors. Adding to this complex scenario, the conflict in Ukraine has destabilized European energy markets, while ongoing COVID-19 related shutdowns continue to hinder China’s economic progress. For developing nations, this strengthening dollar translates into a cascade of challenges: rising import costs, amplified inflationary pressures, escalating debt servicing burdens, increased borrowing expenses, and deteriorating fiscal and current account balances. These factors collectively undermine the prospects of a robust economic recovery from the pandemic’s lingering effects.

The Ripple Effect: Currency Depreciation and Capital Flight

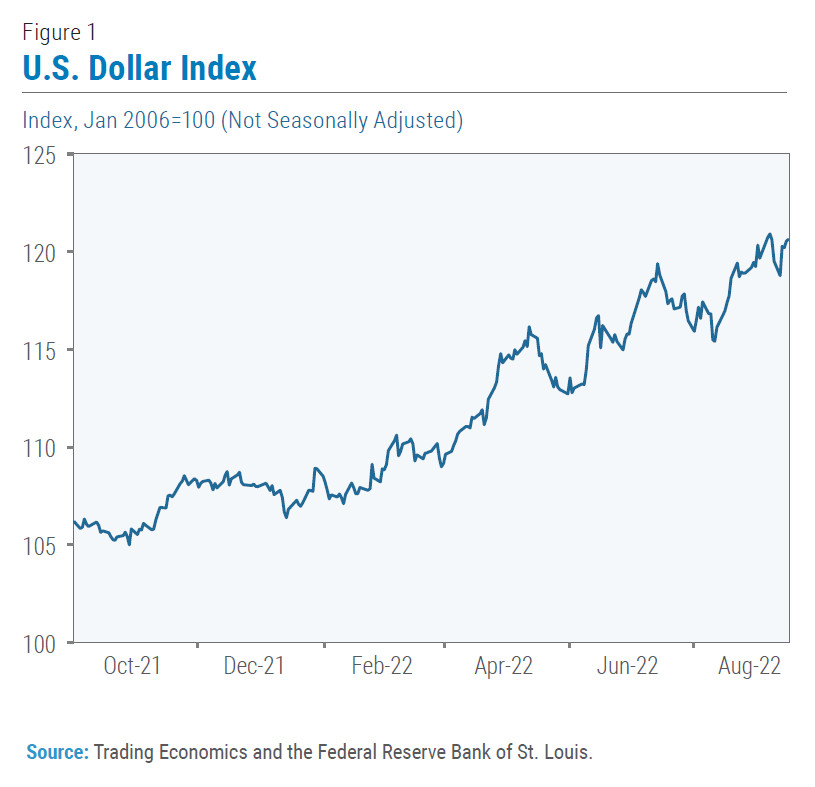

Over the past year, the U.S. dollar index has experienced a remarkable climb of approximately 20 percent against a spectrum of global currencies (Figure 1). Notably, between June and September of this year, the dollar index reached historic peaks as the Federal Reserve implemented substantial policy rate increases totaling 225 basis points. This aggressive monetary tightening has created a global interest rate shockwave, prompting capital to flow out of developing economies. This capital flight is primarily driven by the allure of higher yields on long-term government bonds in advanced economies and investors seeking safer havens for their assets. Consequently, between March and July 2022, developing and emerging markets witnessed an outflow of nearly US$ 32 billion.

U.S. Dollar Index Climbs Amidst Interest Rate Hikes and Global Uncertainty

U.S. Dollar Index Climbs Amidst Interest Rate Hikes and Global Uncertainty

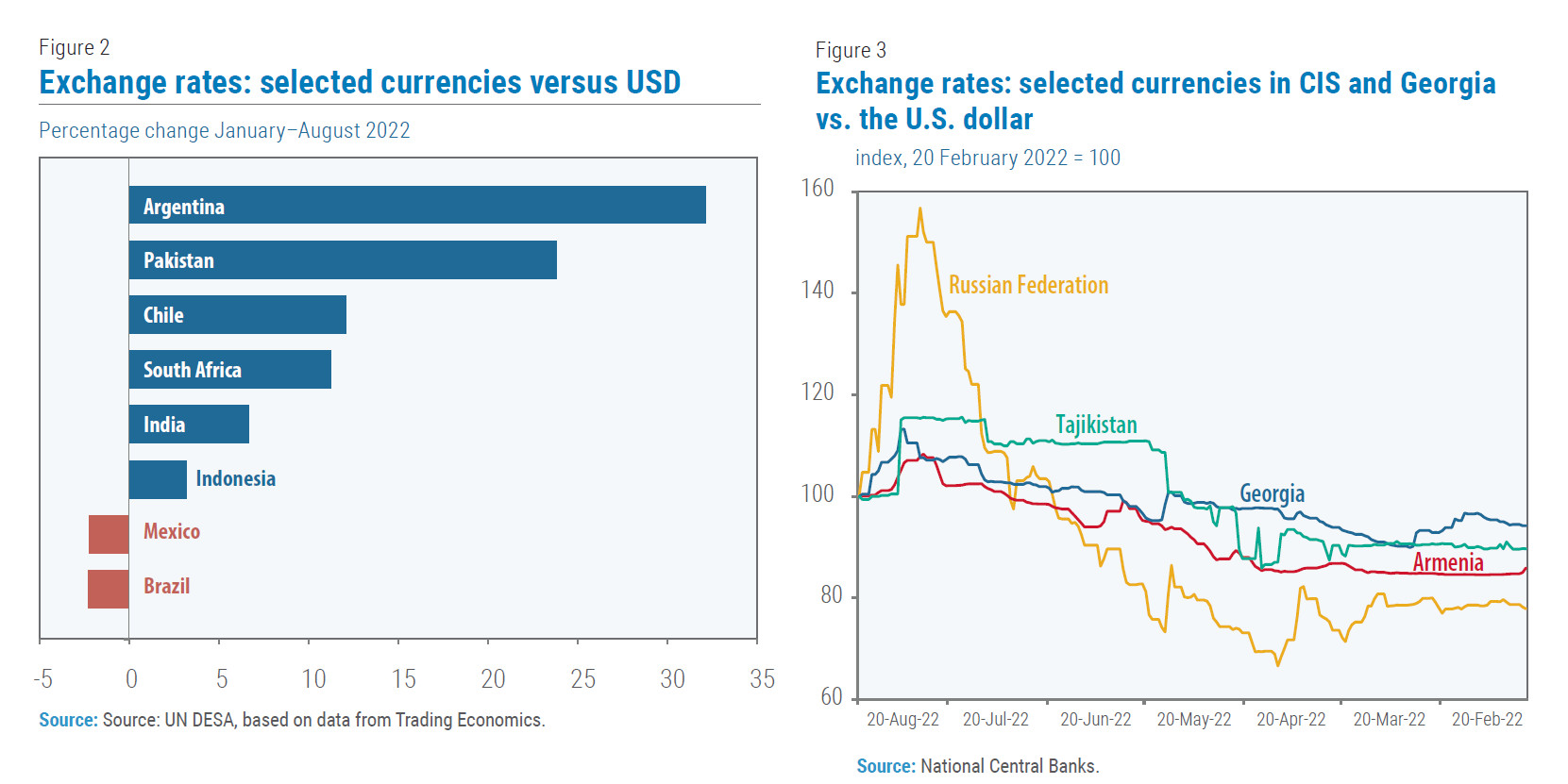

This exodus of capital, combined with international investors reducing their exposure to developing markets, has led to significant currency depreciation in many developing countries relative to the U.S. dollar throughout 2022. Countries like Argentina, Pakistan, South Africa, India, and Indonesia have seen their currencies – the peso, rupee, rand, rupee, and rupiah respectively – weaken considerably against the dollar since the year’s beginning (Figure 2). Interestingly, some Latin American currencies, such as the Mexican peso and the Brazilian real, have shown resilience, buoyed by stronger commodity prices during the first half of 2022. In response to these pressures, many central banks in developing nations have actively intervened to slow down currency depreciation by deploying their foreign-exchange reserves. However, for some economies, particularly those with limited liquid reserves, managing this currency adjustment has proven to be a significant challenge.

Anomalies in the Currency Current: Bucking the Strong Dollar Trend

While a broad trend of dollar appreciation prevails, several currencies within the Commonwealth of Independent States (CIS) have defied expectations, appreciating against the U.S. dollar. The Russian ruble, despite an initial plunge following the onset of the war in Ukraine and subsequent economic sanctions, staged a remarkable recovery. Paradoxically, it emerged as the best-performing global currency in terms of appreciation against major currencies (Figure 3). This surge occurred despite Russia facing double-digit inflation and economic contraction, with half of its central bank’s overseas reserves frozen.

This counterintuitive phenomenon is a result of a confluence of factors. Following the ruble’s initial decline, the Russian central bank drastically increased its policy rate and imposed stringent capital controls. Furthermore, the government mandated exporters to sell a significant portion of their foreign exchange earnings on the domestic market, thereby bolstering demand for the ruble. Adding to this, European gas importers were required to convert their payments to the Russian gas supplier into rubles. Concurrently, Russia’s current account balance improved due to elevated hydrocarbon prices and increased oil exports to Asia, while imports contracted due to sanctions. Consequently, Russia’s current account surplus reached an estimated US$183.1 billion in January–August 2022, a substantial increase from the US$60.9 billion recorded during the same period last year. Similarly, many CIS currencies initially depreciated sharply after the Ukraine war began, but this trend reversed quickly with significant capital inflows from Russia. Many CIS countries and Georgia absorbed substantial capital inflows from the Russian Federation. For example, money transfers from Russia to Armenia almost tripled in the first half of 2022 compared to the previous year, exceeding US$1 billion. This influx is partly attributed to Russian nationals and businesses, including the export-oriented IT sector (often paid in dollars), relocating to these countries. However, this trend is likely temporary, and these nations may face considerable downside risks if these flows reverse.

Currency Depreciation Against the U.S. Dollar in Select Developing Economies

Currency Depreciation Against the U.S. Dollar in Select Developing Economies

Debt Distress Deepens: The Dollar’s Impact on Developing Nations’ Liabilities

A stronger dollar poses a significant threat to developing countries, largely because their external debt and debt service obligations are predominantly denominated in U.S. dollars. While developing country governments collect revenue in their local currencies, a substantial portion of their external debt servicing is required in foreign currencies, primarily U.S. dollars. Consequently, when a domestic currency depreciates against the dollar, a nation’s debt service burden can increase proportionally without a corresponding rise in tax revenue. Developing countries with high levels of external debt are particularly susceptible to sudden tightening of global financial conditions. Many governments in these nations rely on short-term borrowing from international capital markets to meet long-term debt repayment commitments.

Composition of External Debt Denominated in U.S. Dollars Across Regions

Composition of External Debt Denominated in U.S. Dollars Across Regions

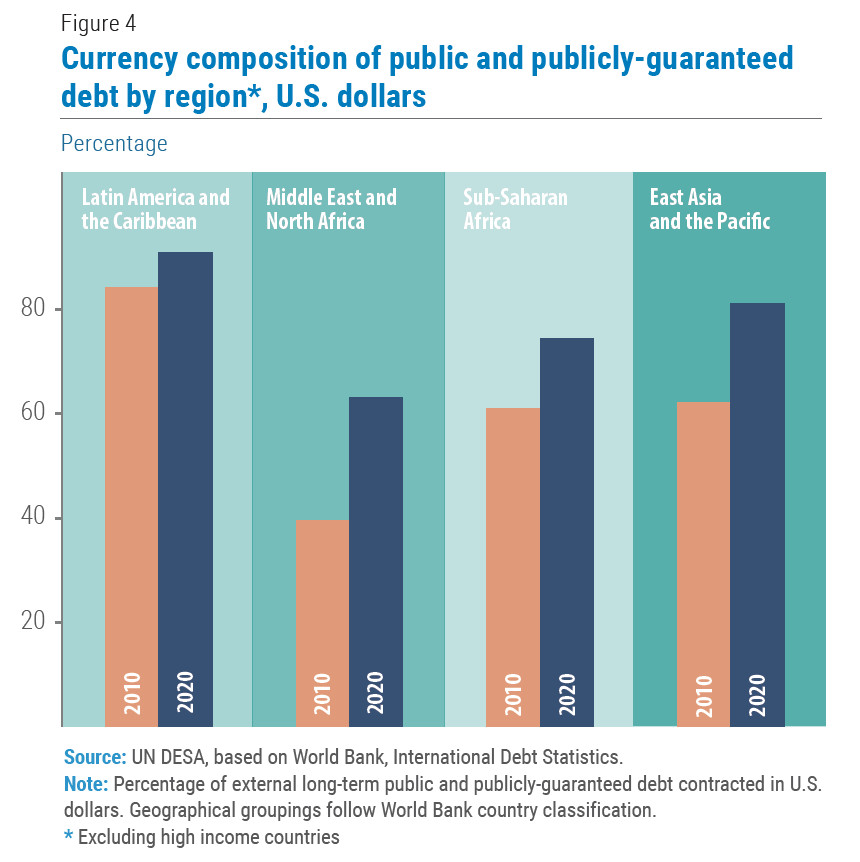

In the decade preceding the COVID-19 pandemic, developing countries benefited from robust capital inflows, especially in Asia and Latin America. Low interest rates and abundant global liquidity encouraged many to borrow from international capital markets, leading to a surge in external debt. Furthermore, fiscal measures implemented to mitigate the economic fallout of COVID-19 pushed debt levels in some countries to unprecedented highs. According to the World Bank, the external debt stock of low- and middle-income countries rose by an average of 5.6 percent in 2020, with many experiencing double-digit increases. Significantly weakened exchange rates, tighter global financial conditions, and sluggish economic growth have amplified debt risks and vulnerabilities across developing countries. The most vulnerable are those where foreign currency-denominated debt constitutes a large proportion of their exports. For some nations, meeting interest payments to creditors has become exceptionally challenging, particularly those facing substantial currency depreciations. The proportion of dollar-denominated debt varies significantly across regions (Figure 4). The Middle East and North Africa have a relatively lower share compared to other regions, while in Latin America, it reached approximately 90 percent in 2020.

Growth Under Pressure: The Broader Economic Consequences

Beyond debt burdens, a strong dollar can also impede long-term economic growth in developing countries by increasing the cost of capital and dampening both public and private investment. As the U.S. Federal Reserve raises interest rates, central banks worldwide often follow suit to prevent capital outflows and mitigate downward pressure on their exchange rates. However, these interest rate hikes increase domestic borrowing costs, thereby reducing both public and private sector investments within their economies.

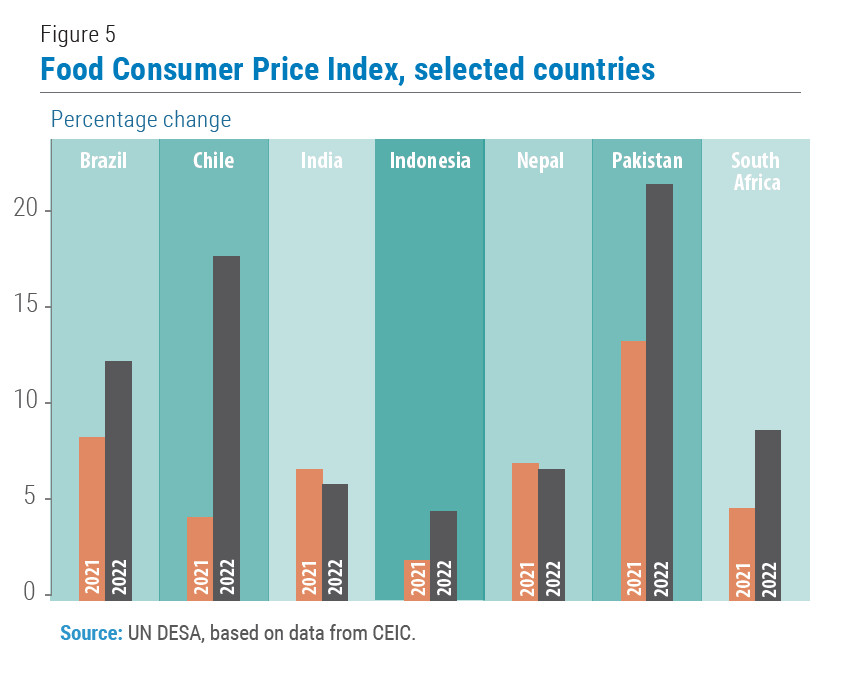

A strong dollar also inflates import prices, especially for developing countries heavily reliant on imports to meet domestic food and energy demands. The majority of international trade is conducted in U.S. dollars. Between 1999 and 2019, the U.S. dollar accounted for 96 percent of trade invoicing in the Americas, 74 percent in the Asia-Pacific region, and 79 percent in the rest of the world. Europe, where the euro is dominant, remains the primary exception. While a strong dollar can help curb inflationary pressures within the United States, it has the opposite effect on inflation in developing economies that are net importers of food and energy. In the current geopolitical climate, a stronger dollar is undermining food and energy security in many developing countries, as import prices for essential commodities like food grains and oil—when denominated in local currencies—have risen sharply in recent months.

Inflation Pass-Through from Exchange Rate Depreciation to Domestic Prices

Inflation Pass-Through from Exchange Rate Depreciation to Domestic Prices

The “pass-through effect” of a domestic currency’s depreciation against the U.S. dollar varies depending on country-specific characteristics. Generally, greater openness to trade and financial transactions, less credible central banks, more volatile inflation and exchange rates, and lower levels of market competition are associated with higher pass-through effects on inflation. Empirical evidence suggests that economies with higher exchange rate pass-through to domestic prices and significant dollar-denominated debt face a difficult policy trade-off between stabilization and inflation management when confronted with adverse external shocks. The policy challenges for developing countries are now even more formidable. Limited room for maneuver exists given persistent supply-side bottlenecks that are exacerbating inflationary pressures and high levels of dollar-denominated external debt.

Dollar’s Dominance: How Long Will It Last?

As indicated following its FOMC meeting on September 21st, the U.S. Federal Reserve intends to raise its key policy rate to 4.25–4.4 percent by the end of 2022. These rate hikes are likely to continue into at least the first half of 2023, with substantial and detrimental spillover effects on developing countries already grappling with a downward spiral of slow growth, high inflation, and high unemployment. The deteriorating economic outlook for developing countries is likely to further weaken their exchange rates in the near term, intensifying capital outflows and further worsening their financing conditions. Against this backdrop, many developing countries face a significantly challenging uphill battle to achieve robust recovery, stimulate growth, and make meaningful progress towards the Sustainable Development Goals (SDGs).

References

Monthly Briefing on the World Economic Situation and Prospects, United Nations Department of Economic and Social Affairs (UN DESA).

Monthly Briefing | News & Events | Global Macroeconomic Prospects | Global Economic Monitoring Branch (GEMB) | Monthly Briefing on the World Economic Situation and Prospects